When business owners think about credit, they often jump straight to banks, credit cards, or loans. But one of the most overlooked and powerful tools for building a strong business credit profile is trade credit. By working strategically with vendors and suppliers that extend net-30 or net-60 terms and, more importantly, report payment history to business credit bureaus, you can establish and grow your company’s creditworthiness faster than through many traditional avenues.

In today’s digital-first era, where AI and fintech tools streamline vendor payments and reporting, unlocking trade credit is not just a matter of convenience but a critical growth strategy.

In this piece, we take you through the importance of trade credit in building a strong business credit profile as an alternative to traditional loans and credit cards, and how to get vendors to report your payment history to credit bureaus. Additionally, we discuss how to use AI tools to manage vendor credits, leverage trade credit for business growth, and turn trade credit into a competitive advantage.

Before we continue, if you are an online business owner struggling with sales, or want to make money online and need free training tools and tactics to set your business on the path to success and profitability, click on the following link to join our free membership clubs. Whether you are stuck on traffic, struggling with content, or do not even know what to sell, there is a solution here.

Why Trade Credit Matters More Than Ever

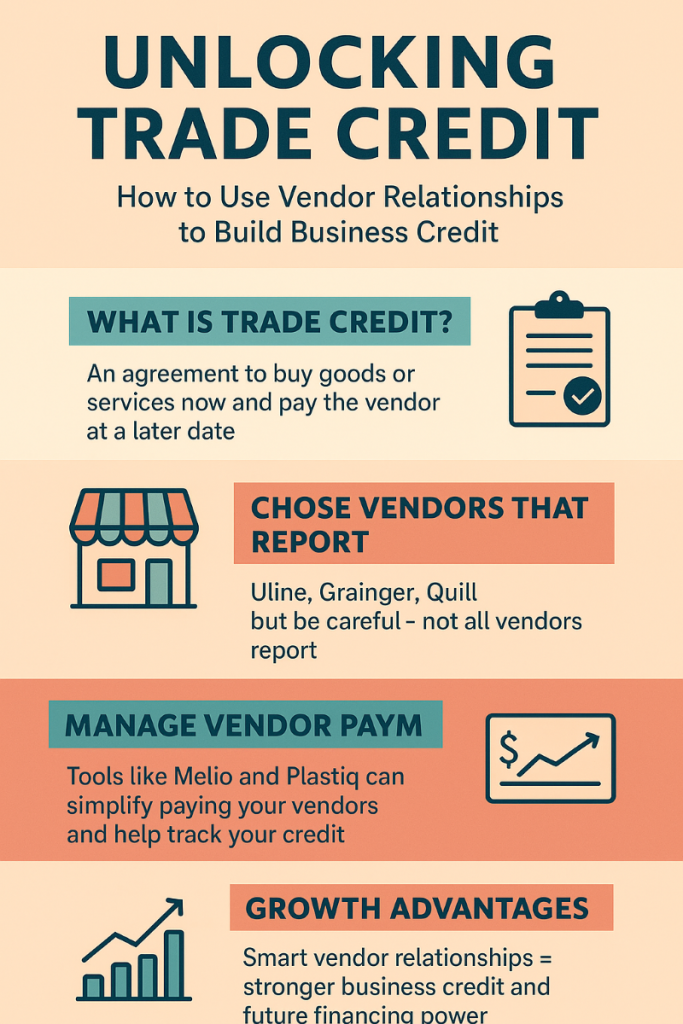

Trade credit is simple in concept: vendors supply your business with goods or services upfront, and you pay them back later—often within 30 to 60 days. This arrangement improves cash flow, but its real power lies in how it builds your business credit profile. Each on-time payment signals to the credit bureaus that your company is reliable and trustworthy. Over time, these positive signals strengthen your business credit score, which in turn makes it easier to access loans, secure better financing terms, and negotiate with new vendors.

In uncertain economic markets, when lenders are tightening traditional credit, a strong vendor credit history can be the bridge that keeps operations running smoothly. It not only gives your business breathing room but also creates a financial reputation that banks and fintech lenders recognize as low-risk.

Choosing Vendors That Count Toward Business Credit

Not all trade credit is created equal. Many small businesses work with vendors that do not report payment history to credit bureaus, which means the opportunity to build credit is lost. The key is to be selective about vendors. Net-30 and net-60 vendors like Uline, Grainger, and Quill are well-known for reporting payments to bureaus such as Dun & Bradstreet, Experian Business, and Equifax. By prioritizing relationships with vendors that report, you ensure every dollar you spend is also working to grow your credit profile.

This is where technology becomes a partner. AI-driven platforms like Nav aggregate your business credit data across multiple bureaus and track how vendor payments are influencing your profile. Instead of guessing whether your trade credit is working for you, Nav provides visibility into the actual impact, along with tailored recommendations on how to strengthen your credit further.

Managing Vendor Credit with Smart Payment Tools

Building vendor credit is not just about having accounts; it is about managing them wisely. The worst thing you can do is miss a payment deadline, which not only erases the benefits of trade credit but also damages your business credit profile. This is where AI-enhanced payment platforms step in.

Melio has become a favorite among small businesses for its ability to automate vendor payments. With Melio, you can schedule payments to vendors in advance, choose how funds are delivered (bank transfer, debit, or even credit card), and ensure that every bill is paid on time. By reducing the human error element of accounts payable, Melio strengthens your credit-building strategy.

Another useful tool is Plastiq, which allows businesses to use credit cards to pay vendors that do not normally accept them. This not only improves cash flow but also ensures that vendor relationships remain consistent and reliable. Together, these tools make managing multiple vendor accounts more efficient, turning credit building into a structured and dependable process.

Leveraging Trade Credit for Growth

Once your vendor relationships are established and your business credit begins to improve, trade credit can unlock more than just financing opportunities. A solid business credit profile creates leverage. You can negotiate better terms with suppliers, ask for higher credit limits, and reduce upfront costs. Vendors are more likely to extend flexibility to businesses that have proven themselves trustworthy over time.

In addition, stronger credit opens doors to external financing when it is needed most. Lenders—both traditional banks and fintech platforms like BlueVine —look favorably on businesses with consistent vendor payment histories. What starts as a small line of vendor credit can ultimately serve as the foundation for larger growth capital.

AI and Predictive Finance in Vendor Credit Management

The role of AI in trade credit is rapidly expanding. Platforms like Fathom and QuickBooks Online Advanced integrate vendor payment tracking with predictive financial analytics. This means you can forecast cash flow needs weeks in advance and align them with upcoming vendor payments. By doing so, you avoid late payments and preserve the positive reporting that builds your credit profile.

These predictive insights also help you optimize working capital. Instead of paying all invoices at once, AI tools can stagger payments strategically to maximize liquidity while keeping every vendor satisfied. This smarter approach to vendor management ensures your credit-building strategy does not come at the expense of day-to-day operations.

Before we conclude, if you are looking to start an online business that is Done For You with ongoing support, or you want to make money online but do not know where to start, then look no further. Click on the following link and learn more. To your success.

https://SteveAikinsOnline.com/survey.php

Conclusion: Turning Trade Credit into a Competitive Advantage

The truth is, many business owners overlook trade credit because it does not feel as glamorous as securing a bank loan or raising capital from investors. But in practice, trade credit is one of the fastest and most accessible ways to build a business credit profile. It is often available to businesses with limited history, requires no collateral, and—when managed well—opens the door to much bigger opportunities.

In this AI era, the businesses that thrive will be those that treat vendor relationships as strategic assets, not just transactional ones. By aligning with vendors that report to bureaus, leveraging AI-powered payment platforms like Melio and Plastiq, and monitoring progress with analytics tools, you can unlock trade credit as a cornerstone of financial growth.

The smartest founders are not waiting for traditional lenders to validate them. They are building their creditworthiness day by day through vendor trust, and in doing so, they are creating businesses that are not only creditworthy but also resilient in uncertain markets.

The author, Stephen Aikins, has over two decades of experience working in various capacities in financial and business management, government, and academia. As a seasoned financial and management professional with a wealth of experience spanning diverse industries, he provides AI-powered digital solutions with data-driven insights to help enhance business growth. Additionally, he has prior experience offering strategic guidance and practical solutions to address a wide range of challenges and opportunities, including auditing and financial analysis, business planning, and organizational development.

The information presented in this blog is based on the author’s independent research and is for educational purposes only. At the time of writing, the author is not affiliated with any vendors of the AI tools and platforms mentioned in this blog. The links to these AI tools and platforms have been presented in the blog to enable readers to access, research, and make their own informed decisions.